What is Life Insurance?

Life insurance is a contract between an insured and an insurance company.

How Much Life Insurance Do I Need?

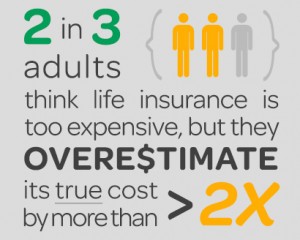

There is no cookie cutter answer. Fundamentally, life insurance is a way to provide protection against the economic loss caused by the death of the insured. Personal circumstances dictate what additional questions need to be answered, such as how many years of income should be replaced or are there beneficiaries with special needs or other lifestyle considerations.

Why Do I Need Life Insurance?

Income replacement: For most people, their key economic asset is their ability to earn a living. If you have dependents, then you need to consider what would happen to them if they no longer have your income to rely on.

Final Expenses: Proceeds can be used for funeral and burial costs, and medical expenses not covered by health insurance. Since life insurance contracts usually pay very quickly, the proceeds could be used to bridge the gap between the time the insured dies and the time other sources of money get freed up.

Final Expenses: Proceeds can be used for funeral and burial costs, and medical expenses not covered by health insurance. Since life insurance contracts usually pay very quickly, the proceeds could be used to bridge the gap between the time the insured dies and the time other sources of money get freed up.

Pay outstanding debts and long-term obligations: Properly structured life insurance policies can be used for a variety of circumstances, while the insured is still alive. Cash value life insurance can be used to pay off debt like credit cards, medical bills, car loans, student loans and mortgage.

Estate planning: The proceeds of a life insurance policy can be structured to pay estate taxes so that your loved ones will not have to liquidate other assets.

Supplemental Retirement Income: Here again a properly structured life insurance policy can provide supplemental retirement income, often tax free. This may be useful in situations like retiring early or waiting before tapping social security.

Charitable Contributions: If you have a favorite charity, you can designate that some or all of the proceeds from your life insurance go to that organization.

Types of Life Insurance

Term Life Insurance

Term Life insurance, is the lowest cost life insurance. It provides a death benefit and has no cash value. Typically the premium you pay is guaranteed for a specified term (hence the name) such as 10, 20 or 30 years. After the guaranteed term is up, the premium increases enough to be painful so most people drop it.

Universal Life

Universal Life is a flexible-premium, adjustable-benefit life insurance contract which may or may not accumulate cash value. Flexible premium means that (subject to certain limitations) the policy owner may pay more or less than the premium stated in the contract. Depending on certain factors, premium payments could be skipped in particular years at the policy owner’s discretion. The adjustable benefit allows you, the policy owner to increase or decrease the stated death benefit, subject to certain guidelines. How much you pay or skipping payments could have an impact on how long the policy will last. Life insurance that lapses cannot help any of your loved ones.

Universal life comes in multiple styles mostly related to how the cash value grows.

Whole Life

Whole Life is the most basic type of permanent life insurance. Your premium will purchase a specific death benefit and produce a specific cash value, which are guaranteed for the life of the policy as long as the premiums are paid. Whole Life premiums are usually higher than term premiums, and are guaranteed not to increase.

Why Should I Work With a Life Insurance Agent?

While it is possible to find and apply for life insurance online, you should seek the help of a life insurance professional to help you with the process. Working with an agent will not cost you anything since the agents are paid by the insurance company. Life insurance rates are set by the company and registered with each state the company does business in. The companies can’t give you a lower rate for buying direct. An agent will be able to guide you through the process.

Bruce Kuczinski is Founder and President of Solutions for Wealth, Inc. which specializes in safe money alternatives to retirement income planning. Bruce has been active in financial services since 2003.

Bruce can be reached at 321.574.0440

or on the web at : solutionsforwealthinc.com